.jpg)

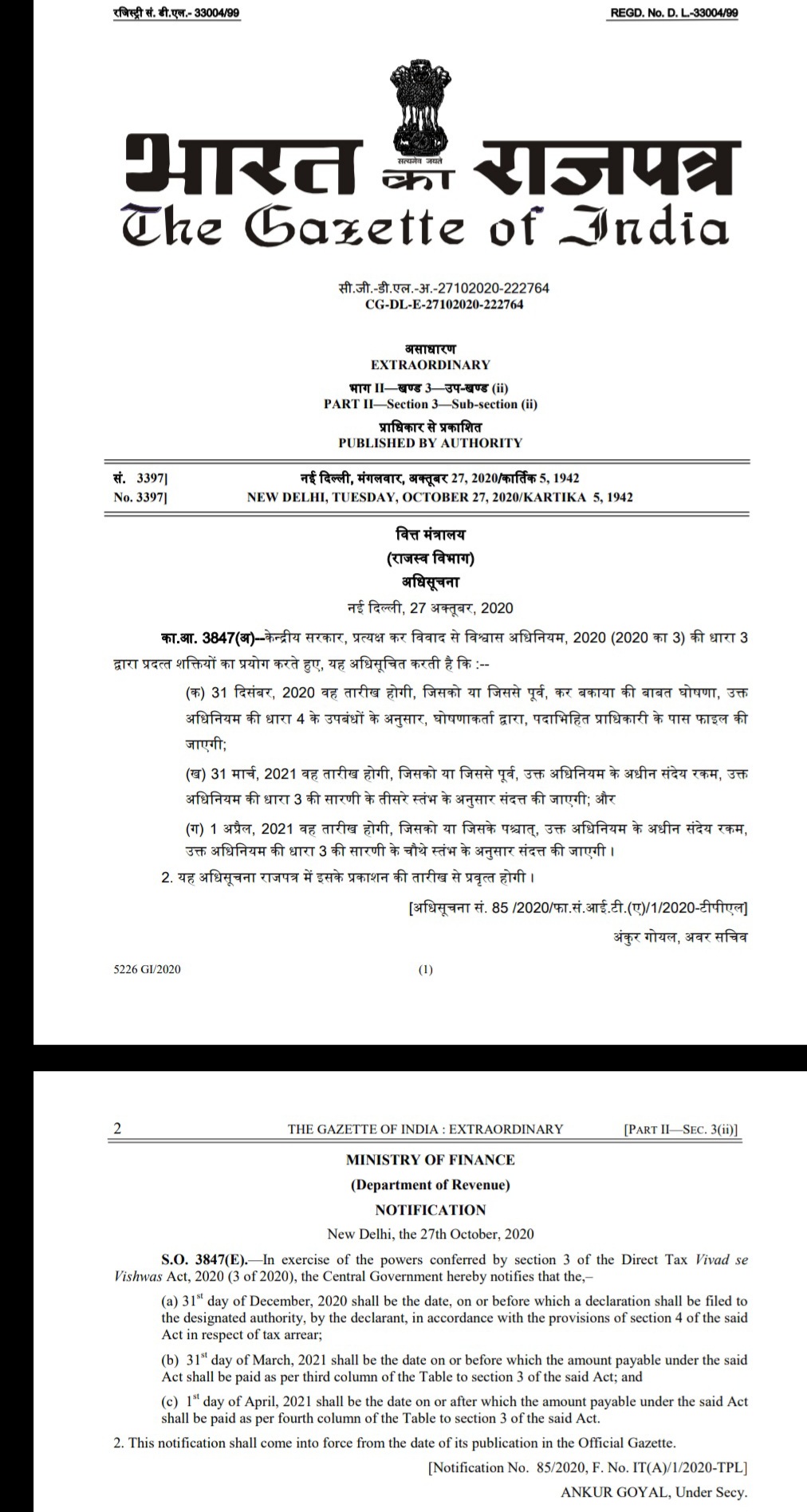

CBDT further extends the last date for making payment under Vivad se Vishwas Scheme and also notifies the last date for filing Declaration in Form 1 under the Scheme

In exercise of the powers conferred by section 3 of the Direct Tax Vivad se Vishwas Act 2020, the CBDT vide its Notification No. S.O. 3847(E) dated 27.10.2020, have further extended the last date for making payment of disputed tax without additional amount under the Vivad se Vishwas Scheme, from 31st December, 2020 to 31st March, 2021.

Further, the Declaration in Form 1 u/s 4 of the Act, for opting for settlement of income tax disputes under the Vivad se Vishwas Scheme, are required to be filed electronically, latest by 31st December, 2020.

Therefore, as per the above amendment as prescribed in the CBDT Notification, the revised due dates for payment of tax payable under section 3 of the Direct Tax Vivad se Vishwas Act 2020, by the Declarant are as under:

(I) Where the Appeal/Writ Petition/SLP has been filed by the Declarant

|

Nature of Tax Arrear |

Amount payable on or before 31.03.2021 |

Amount payable on or after 01-04-2021 |

|

Aggregate of disputed tax, interest chargeable and penalty on such disputed tax, in cases other than search/block assessments |

100% of the amount of disputed tax |

110% of the amount of disputed tax. |

|

Aggregate of disputed tax, interest chargeable and penalty on such disputed tax, in cases of block assessment u/s 153A/153C, assessment u/s143(3), reassessment u/s 148, pursuant to a search action u/s 132, where disputed tax is less than Rs 5 crores |

125% of the amount of disputed tax |

135% of the amount of disputed tax. |

|

Aggregate of disputed tax, interest chargeable and penalty on such disputed tax, in cases where the declarant/assessee has got a favourable decision in earlier assessment years from the higher appellate authorities and such favourable decisions have not been reversed. |

50% of the amount of disputed tax |

55% of the amount of disputed tax |

|

Aggregate of disputed interest, penalty and disputed fee |

25% of such disputed interest, penalty or fee |

30% of such disputed interest, penalty or fee |

(II) Where the Appeal/Writ Petition/SLP has been filed by the Income Tax Authority

|

Nature of Tax Arrear |

Amount payable on or before 31-03-2021 |

Amount payable on or after 01-04-2021 |

|

Aggregate of disputed tax, interest chargeable and penalty on such disputed tax, in cases other than search/block assessments |

50% of the amount of disputed tax |

55% of the amount of disputed tax. |

|

Aggregate of disputed tax, interest chargeable and penalty on such disputed tax, in cases of block assessment u/s 153A/153C, assessment u/s143(3), reassessment u/s 148, pursuant to a search action u/s 132, where disputed tax is less than Rs 5 crores |

62.5% of the amount of disputed tax |

67.5% of the amount of disputed tax. |

|

Aggregate of disputed interest, penalty and disputed fee |

12.5% of such disputed interest, penalty or fee |

15% of such disputed interest, penalty or fee |

{kind=link}